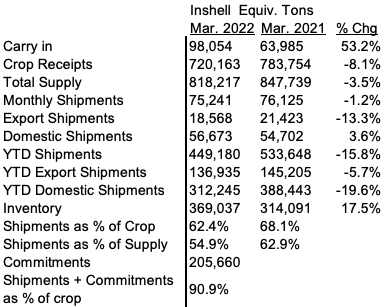

The California Walnut Board March 2022 Position Report is below. Total March shipments were down -1.16% vs PY with March domestic down -13.3% and March exports up 3.6%. YTD shipments are down -15.8% vs PY with YTD domestic down -5.7% and YTD exports down -19.6%. See the attached Position Report from the California Walnut Board with summary table.

YTD Domestic sales are decent at 136,935 ton down -5.7%

YTD Export sales are weak, 312,245 ton down -19.6% from 388,443 prior year

- Turkey, at 61,749,820 pounds down -42.1% from 106,688,645 prior year

due to high prices and a massive decline in the Turkish Lira. Others of note were India (-81%), UAE (-54%), Algeria (-80%), Italy (-16.6%), Spain (-17.4%).

- Shippping channels, while improving a bit are still tough. If the lanes open up, there could be some decent months going forward but the bottlenecks are frustrating and leave some many open questions and buyers have missed various windows, holidays and seasons giving overseas buyers excuses to ask for discounts or cancellations.

- Inshell Chandlers are very difficult to find so buyers will look ahead to pricing from Chile as California is largely sold out.

- Purchase Commitments are calculated as 205,660 Inshell ton. Purchase Commitments plus shipments are (449,180 + 205,660 = 654,840 inshell ton) which is 90.93% of total 2021/2022 crop receipts and 80% of total supply.

- CARRY OUT – Using YTD actual sales through March 2022 and using last year’s monthly April 2021 through August 2021sales of 216,716 inshell ton as a estimate, the forecast is 152,000 inshell equivalent ton of carry out compared with prior year carry out of 98,054 inshell ton or up 55%. However, with the Purchase Commitments at 205,660 inshell ton, the industry is holding a tremendous amount of goods that are sold, just not shipped yet. If these goods can find vessels and actually ship, the carry over could be substantially less.

Chile:

Chilenut released Final 2021 Walnut shipment report with shipment of 148,152 tons compared to last year of 131,171 tons an increase of 13%. For the 2021 season; UAE up 19%, Turkey up 49%, China down 42% and India up 85% compared to last year. Chile is expecting 2022 crop to be 175,000 tons an increase of 18%

Prices:

Inshell:

- 30-34mm (JL chandler) at $2.60/kg FOB ($1.18/lb)

- 34+ at $3.20/kg FOB ($1.45/lb)

Kernels:

- 80% LHP at $7.40/kg FOB ($3.35/lb)

- 60% LHP at $7.10/kg FOB ($3.22/lb)

- Hand cracked 90% Extra Light Halves at $10/kg FOB ($4.53/lb)

Duty:

- Turkey has additional 16 cents per lb duty for USA walnuts vs Chile

- Europe has 5.1% additional duty for USA walnuts vs Chile

- UK has 4% additional duty for USA walnuts vs Chile

We are finally starting to see retailers lowering prices after many months of holding the line on prices and margins and now passing on the savings to consumers.

The domestic market is largely uncontracted at this point. Pre-rain Chandler material has started to get tight and has firmed a dime in the past two weeks. Domestic LHP and Combo Halves and pieces have also firmed a dime to follow suit but packers typically get antsy when it gets hot and we will get into the “dog days” of Spring and Summer. We expect sellers to make the decision to sell walnuts instead of putting into cold storage so some deals will come up on Combo and Domestic LHP.

How did we get here? We got here through a combination of:

- A false sense of security

- Inaccurate NASS Forecast

- High Opening Prices

- Bad weather

- Competition

A FALSE SENSE OF SECURITY

2020 actual sales of 748,323

2020 actual crop receipts of 783,754

Sold 95.5% of the crop

INACCURATE NASS FORECAST

True receipts to date 720,163 ton

7.5% higher actual receipts than estimate

What we thought:

NASS estimate of 670,000 was -14.5% from previous receipts of 783,754

NASS estimate of 670,000 was -10.5% from previous sales of 748,323

THE INDUSTY WRONGLY THOUGHT SUPPLY WAS NOT GOING TO BE ENOUGH. THEREFORE PRICES WERE SET PRICES TO HIGH.

ACTUAL RECEIPTS TO DATE OF 720,163 ARE ONLY -8.1% LOWER THAN LAST YEAR’S 783,754 TON

POOR JUDGEMENT ON OPENING PRICES

Original Walnut Market pricing coming out of the California Exporters Association (early September 2021) approximately $3.00/lb CHP, $3.25/lb LHP, $3.45 Chandler LHP, $4.00/lb Chandler Halves, $1.40/lb Chandler Jumbo Large Inshell. The Association believed that the walnut industry was in the driver’s seat due to large sales of 748,323 inshell ton prior year. Today, pre rain Chandler LHP is in the $2.20 to $2.30/lb range with CHP in the $1.60 to $1.70/lb range with Domestic LHP in the $1.85 to $1.85/lb range.

COLD STORAGE

This season is upon us and the valley is within 2-3 weeks of 85 degree days and there is not enough cold storage to go around. No one wants to spend “good money after bad” and there are talks of a number of packers that will need to find large amounts of cold storage or putting product at risk.

Forecasted New Crop

We know that the prior year crop was 783,754 inshell ton and some believe that this upcoming crop will be 780,000 to 800,000 ton. At 2 inshell ton an acre times the number of acres, yields 800,000 inshell ton.

Bad Weather

Late Season Rains – Late rains hurt an estimated 8% of the Chandler crop much of which increased the amount of “combo” product and decreased the amount of export quality Chandler LHP and Halves. Much of the carry over will be in the Combo Halve and Piece category.

COMPETITION

China Quality and Chilean Quality – Chilean Quality is excellent and generally regarded as higher quality then California Chandler variety. Chilean Chandler Halves are going for approximately $3.26/lb FOB so about 10% more than our Chandler Halves today which are $2.90 to $3.00/lb. Inshell is about $1.13/lb FOB, again, slightly higher. Duties on USA walnuts reduces this difference. The question we all have is China. The Chinese Variety “185 Type” which is very nice and drawing praise and accepted in many parts of the world. Will this grow in popularity going forward and at a cheaper price? Photos received of this variety are of excellent quality and seems like gone are the days of the astringent, veined skin, pungent walnuts of the past. This variety is of good quality, similar to California Chandler.

DECLINING MARKET

Declining Market – As the market started to decline from the opening, buyers were happy that they were correct to forecast the market to decline but still were skeptical as to “when to jump back in”. One of the most important pricing skills is for the industry to price the opening price at a level where it slowly rises over time. Even if they leave money on the table for the first couple months is better than dealing with a falling market as buyers are slow to return and really have no idea about when or what to book. How to accomplish that is a different matter.

EXPORT ISSUES

Exports bogging down – Exports are taking longer to go out, many vessels “rolled” or “consolidated” thus increasing transit times and increasing cash collections times for both Export and Domestic. Some packers are concerned with overseas’ buyer cancellations (at the higher price levels) due to missing of certain seasons or holidays which are a “perfect” excuse for a default. The shipping lanes are starting to open up a bit and hopefully the “Purchase Commitment” number will decline and turn into actual shipment.

Summary

On both a Macro and Micro level, there were things uncontrollable. The pandemic, transporation logistics (vessels and containers), foreign exchange rates duties or weather are not controllable. The big mistake was the USDA/NASS missed forecasts and thus the high Industry opening prices. China is formidable with their new variety and Chile’s crop is known for quality but we will have a 6 month head start on Chile. The key to the upcoming season is open reasonably with prices that are sustainable if not rising slightly throughout the season. We believe good post quality Chandler halves and Chandler LHP will continue to rise slightly and nice CHP and LHP will hold firm at these slightly elevated prices