JUNE 2019 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

The California Walnut Board released the June 2019 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell equivalent shipments +4.1% vs. PY

– Export inshell equivalent shipments +5.2% vs PY

– Domestic inshell equivalent shipments +3.0 vs. PY

2) Year to date inshell equivalent shipments +9.8% vs. PY

– Export inshell equivalent YTD shipments +7.1% vs. PY

– Domestic inshell equivalent YTD shipments +15.8% vs. PY

MMR DISCUSSION

The Calif. Walnut industry was up +4.1% in June 2019 over PY June 2018. The monthly sentiment overall was quiet but the industry did what it needed to do to keep the momentum and positivity going as we approach new crop. Across the board, Export and Domestic sales were up for the month and combined were up 4.1% thus halting May’s monthly decline of -2.2% vs. PY. Remember, April 2019 was up 17% over PY, March 2019 which was up 26.3% over PY, February 2019 which was up 35.9% over PY and a January 2019 up 38.7% against PY.

Year to date total sales are up 9.8% with Export up 7.1% and domestic up 15.8%. Shipments as a percentage of Crop are now at 92.5% and 84.5% as a percentage of supply.

Analytical Discussion

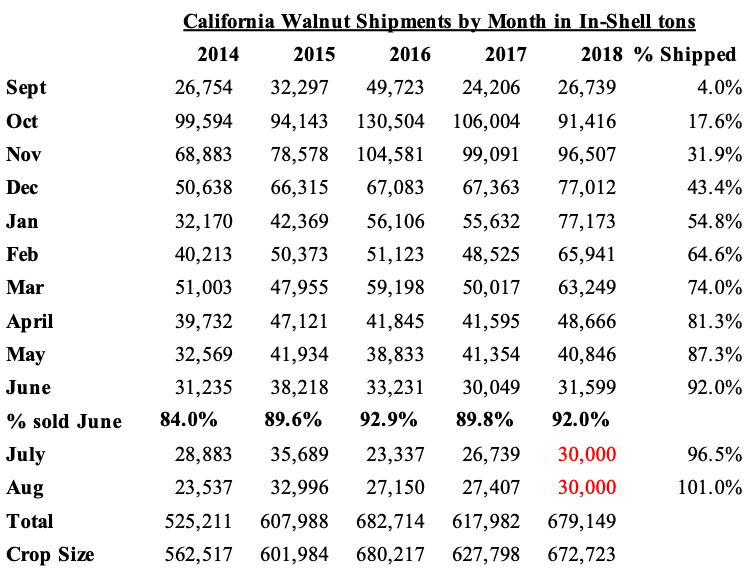

Following last month’s presentation of the below historical table, we’ve added performance for June 2019. With this, the industry is at 92.1% sold based on “crop”. Assuming the next 2 months performance in red, the industry could conceivable sell 101% of the crop thus cutting into to the carryout slightly.

The chart above suggest that for the next 2 months, July 2019 – August 2019, the industry needs to average 30,000 ton of sales each month to move 101% of the crop. The question is whether this last 2 month forecast can be achieved. Nevertheless the industry has moved the crop and is in a good position to start new crop with about the same carry-out as the carry in.

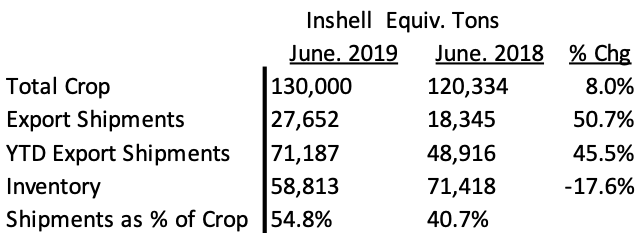

– Chile – Chilenut released June Walnut Position report with record shipment of 27,652 tons compared to last year of 18,345 tons an increase of 51%. June shipments are 11.7% higher then May’s 24,766 tons. For the month of June 2019; UAE up 15%, Turkey is up 52%, China up 618% and India down 14% compared to last year. YTD shipments are 71,187 tons compared to 48,916 tons last year an increase of 46%.

Current price of inshell Chandler is around $3.10/kg CFR and 80% LHP at $8.90/kg CFR. Most Chile packers are sold out and very difficult to find material out of Chile. Dubai is flooded with Chilean material due to current problems in Iran. Buyers are focusing on buying from Dubai and Turkey due to product availability and price. Chile so far shipped 55% of their crop and needs to ship additional 59,000 tons for this season at this rate Chile would have shipped all their walnuts by end August which will be great news for the CA packers as they will not need to compete with Chile when CA starts to ship.

– Existing Inventory – While the crop seems to be well sold, packers still have inventory to sell to turn into cash and finalize payments to growers so, for the time being, there is no shortage of inventory to buy. Most packers have a few loads to sell while some have dozens. Most goods are in cold storage and this helps to motivate packers to stem those unwanted bills. With the well sold position of the industry, one would expect to find shortages of some varieties and sizes shortly.

– New Crop – The recent almond estimate of 2.2 billion pounds has warranted discussion among walnut growers if “the weather that may have caused NASS to lower their estimate on almonds also affected walnuts”. There is continue discussion in the field by packers and growers notating “lower nut cluster counts with more singles and doubles than triples and quadruples”. Most growers say this year’s crop is “moderate and nothing to write home about”. Limited amounts of new crop Chandler Jumbo/Large has been done mostly around $1.15/lb. Overseas bids are in the $1.10/lb range with little interest from packers. New Crop seems to be about two weeks late.

– Pricing for walnut material is slightly lower from our report last month with Domestic LHP $2.40 -$2.60/lb, Export quality 20% LHP $2.85 – $2.95/lb. CHP $2.25/lb to $2.40/lb. Chandler Halves $3.10 to $3.20/lb range with minimal material available. Inshell material is pretty much non-existent.

Conclusion – The historical chart continues to show that the industry is in a strong position to start the new season in late September with about the same amount of carry out as the carry in. Chile’s strong shipments will continue helping to boost California momentum, putting California in very comfortable position in September. What does new crop California walnuts truly look like? It almost is a foregone conclusion that the highest potential of 725,000 ton is not going to happen but is it in the cards that something unexpected like 650,000 ton could happen (similar to almonds)? Don’t count that out as California’s weather is all connected and what hurts one crop generally does not help others. Time will tell.