March 2020 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

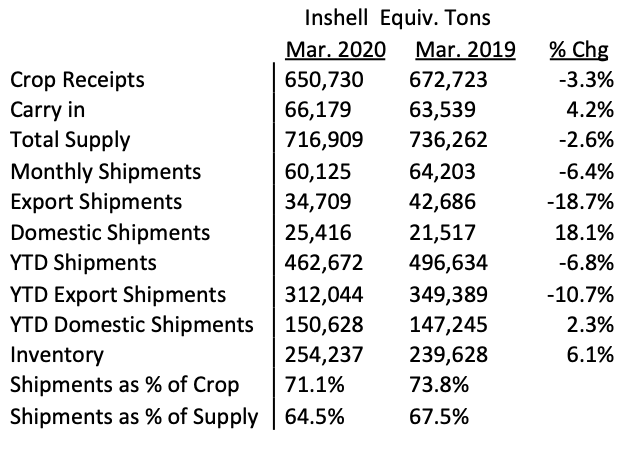

The California Walnut Board released the Mar. 2020 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell (total) equivalent shipments -6.4% vs. PY

– Export inshell equivalent shipments -18.7% vs. PY

– Domestic inshell equivalent shipments up 18.1% vs. PY

2) Year to date inshell (total) equivalent shipments -6.8% vs. PY

– Export inshell equivalent YTD shipments -10.7% vs. PY

– Domestic inshell equivalent YTD shipments +2.3% vs. PY

3) Monthly inshell only shipments -44.9% vs. PY with Domestic -33.75% and Export -45.43%

– Key highlights include Turkey up 14.5% vs. PY, Italy -33.3%, UAE -93.1%, Vietnam up 395%, India +271.2%, Pakistan down 100%.

4) Monthly kernel only shipments -1.0% vs. PY with Domestic +18.5% and Export -12.9%

5) Year to date inshell only shipments -19.77% vs. PY with Domestic -36.2% and Export -19.0%

– Key highlights include YTD inshell shipments to Turkey very close to prior year at -3.9%, up 22.3% to India, -45.4% to UAE, +15.8% to Vietnam, +15.4% to Germany, +0.51% to Italy), +1% to Spain, -99.7% to Pakistan.

6) Year to date kernel only shipments -1% vs. PY with Domestic +3.8% and Export -4.4%

Note that both YTD kernel and the March kernel shipments are very close to being on par with last year. Inshell only shipments have declined substantially for the month and year to date continues to fall further behind at -19.77% YTD.

MMR DISCUSSION

March’s report is a bit of a mixed bag at -6.4% as this is still the second strongest March shipment in history. March Total Domestic sales are decently up 18.1% but total Export is down 18.7%. Export volume is twice the size of Domestic so it hurts more. Monthly Domestic shelled has been strong up 18.5% but Monthly Export Shelled -12.9%, Monthly Domestic Inshell -33.75% and Monthly Export Inshell – 45.43% is disappointing. Similarly, YTD Domestic Shelled up 3.83% is strong but YTD Export Shelled -4.43%, YTD Domestic Inshell -36.2% and YTD Export Inshell – 19% is disappointing.

Packers had been optimistic that sales would be good for March due to the cheaper prices. Many were extremely busy with shipments and the domestic numbers bear that out but the offset was down Export sales of both inshell and shelled.

Covid-19

The virus has undoubtedly has had a negative effect on sales of all walnuts, inshell and shelled, domestic and export, to what extent nobody knows. Domestically, supermarket bulk sales, Foodservice and Restaurants are reeling. Many countries are on lockdown affecting ports domestically and abroad and affecting people’s ability to buy goods and companies’ ability to process goods. Since this virus has never been seen before, it is an unknown if or when it will subside or whether it will be a virus that comes back annually. Hopefully a successful inoculation is forthcoming.

Chilean Walnuts

Chandler harvest started early last week. Crop size is expected to be similar to last year around 130,000 tons. Sizes are smaller as percentage of baby walnuts are expected to be around 15-25% of the crop, double their normal amount. First chandler inshell shipments is sailing this week. Chandler 30mm+ is between $2.65-$2.80/kg CFR. Serr 30mm+ is around $2.80/kg CFR. Chandler 20% LHP is around $7/kg CFR, 80% LHP is $7.45-$8/kg CFR and Hand cracked is between $10-10.50/kg CFR.

Morocco and India have been the biggest buyers of Chilean inshell walnuts so far. Dubai is in full lockdown for 2 weeks. Turkey is waiting for Chile to lower their inshell prices as USA inshell prices looks more attractive. Most Chilean packers have availability for prompt shipments but finding a container has been a challenge for Chile.

Inshell Prices and Kernel Prices

Inshell prices for Jumbo/Large Chandler have recently been done in the $.96/lb to $1.05/lb range. The Large traders were actively bidding at the lower range but most packers were trying to sell at the higher range. It does not seem that prices in the lower inshell range are readily available anymore. Chandler LHP 20’s currently in the $2.70 to $2.80/lb range. Domestic LHP is in the $2.60 – $2.70/lb range and Combo Halves and Pieces in the $2.50/lb to $2.65/lb range. Chandler halves are in the $3.00 – $3.10/lb range. Kernel sales domestically have been good and could have been better if not for Covid-19. Inshell across the board is quiet. Cold storage season will be upon us in 30-45 days which will add additional selling motivation.

Existing Inventory and sales position

Chandler material is still available but the decline in prices seemed to have stopped. CHP is minimal and domestic light product is becoming tougher to find. Yet with most of the packers we talk to at well over 90% sold (compared to the percentage of crop sold vs. supply at 64.5% and as a percentage of crop sold vs. the total crop is 71.1%) and with 41.6% of the season to go to the end of August and at least 6 months to go before any Chandlers are available)…..who has are the players with large amounts of inventory to sell?

The next 5 months for the fiscal season are critical. Last year, April – August 2018-2019 sales were 176,449 inshell ton. If we assume this number for the upcoming 5 months and subtract this number from existing inventory that would leave us carry out of 77,788 ton or an increase in carry out inventory of 17%. If during these 5 months we fall behind by 10% from last year’s sales, then the carryout would be approximately 95,433 or an increase of 44%.

What We Know and Don’t Know

– The crop is final at 650,730 ton.

– Chile’s crop is estimated to be 120,000 – 130,000 ton with inshell prices at about $1.20/lb to $1.27 CFR for Jumbo Large Chandler Inshell.

– Calif. Inshell sales going forward will be very slow. Where does the industry stand with containers on the water or loads still unshipped? If this inshell winds up being cracked, how will the cracking of this inshell inventory affect the kernel market?

– Will the Covid-19 curve around the world flatten out and will people’s lives begin to normalize? Covid-19 seems to be the “catch all excuse” for many things and walnut buyers have tried to use this excuse to their advantage. Almost all packers have felt some pain due to Covid-19’s affect on demand and logistics.

– Cold storage season will begin in May 2020 and will motivate packers to want to move goods out.

– There are rumblings of a large and significant USDA Trade Mitigation Walnut buy coming in the next month. Can this move the needle?

CONCLUSION

The March 2020 MMR report has stoked more fears than to quell them. Covid-19 has not helped and pervasive lock downs have created a pretty somber worldwide atmosphere.

Inshell packers are still trying to get over $1.00/lb for Jumbo Large Chandler on average yet Chilean new crop will be 20% higher on average. Maybe there is a window of optimism for Inshell buyers to buy California Inshell over Chilean Inshell based on the price differential and immediate availability. Looming however is a potentially large 2020 crop in September/October 2020 possibly over 725,000 inshell ton and an almost inevitable carry out of over 90,000 ton. Where lies the remaining 30-35% of the supply and when will this inventory come to market and at what price?

We look forward to any questions, comments or interest you may have and we would be happy to assist you.