May 2020 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

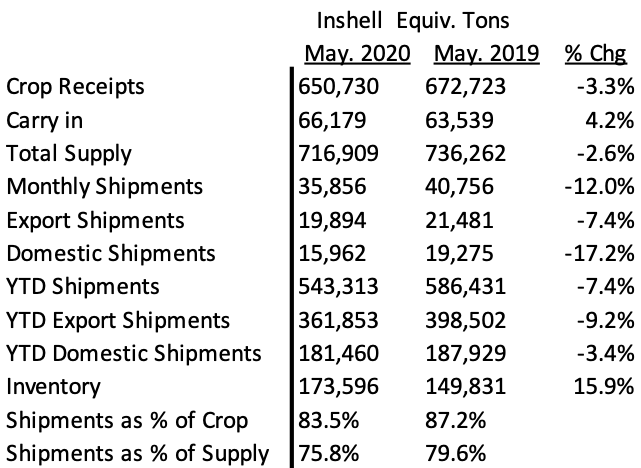

The California Walnut Board released the May 2020 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell (total) equivalent shipments -12.0% vs. PY

– Export inshell equivalent shipments -7.4% vs. PY

– Domestic inshell equivalent shipments -17.2% vs. PY

2) Year to date inshell (total) equivalent shipments -7.4% vs. PY

– Export inshell equivalent YTD shipments -9.2% vs. PY

– Domestic inshell equivalent YTD shipments -3.4% vs. PY

MMR DISCUSSION

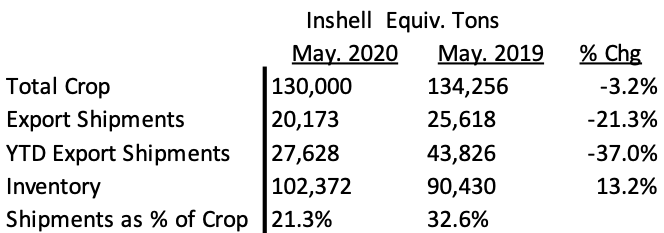

May’s performance was soft at -12%. While May inshell was up 78.4% to 4.8 million inshell pounds (Turkey up 882% to 1.7 million pounds), kernel was down 15.5% from 34.8 million pounds last May 2019 to 29.4 million pounds this May 2020. Domestic and Export kernel were down 16.2% and 14.9%, respectively. As expected Covid-19 and the now 3-4 month lockdowns in many countries hurt sales with little momentum moving forward. California walnut cold storage season started a month ago with many packer’s now selling goods with additional costs for cold storage and added motivation to minimize those costs. Chile has started shipping their new crop walnuts and are at 21.3% shipped as percentage of crop versus 32.6% shipped last year. Hopefully as more countries open up and consumers and countries get back to some sense of normality, we will see an uptick in California walnut sales as prices are fairly attractive.

Chilean Walnuts

Chilenut released May Walnut Position report with shipment of 20,173 tons compared to last year of 25,618 tons a decrease of 21%. For the month of May 2020; UAE down 86%, Turkey down 48%, China up 328% and India up 65% compared to last year. YTD shipments are 27,628 tons compared to 43,826 tons last year a decrease of 37%. Chile so far shipped 21.3% of their crop and needs to ship additional 102,000 tons for this season.

It is rumoured that some U.S. Traders have started offering 95 cents /lb FAS for new crop J/L Chandler inshell. This will most likely hurt Chile who have recently dropped prices to approximately $2.70/kg CFR for top tier packers and $2.60/kg CFR for lower tier packers. 80% LHP at $7.60/kg CFR and Hand Cracked is around $10.50/kg CFR. Chile has started to reluctantly lower prices to try to increase sales and try to move out their crop. California wants this too. California does not want Chile to have significant amounts of product as California begins to harvest non export varietals in September and then Chandler in October 2020. Chile’s colour quality is sub par to normal years due to drought which may help California if it’s colour quality is good compared with Chilean which would also be 5 months older product. It will be a balancing act with Chile looking at California and vice versa.

USDA Trade Mitigation and Domestic Commodity Solicitations

The government just last week concluded another multi million pound trail mix program which included either (almonds or walnuts), raisins, cranberries and cherries. While this solicitation did have the option to allow for walnuts, the almond pricing was more competitive and was thought to be more conducive to the winning bid which was announced June 3rd. It is believed that the government will continue these food programs in which trail mix or straight walnuts will be requested. These programs have been a big help to the California Walnut Industry and have become more and more competitive with more bidders and lower prices. It is believed that these programs will continue month after month and will continue to help walnuts, almonds, raisins, prunes and figs.

Inshell Prices and Kernel Prices

Current crop Inshell prices for Jumbo/Large Chandler are still in the $1.00 to $1.05/lb range. Chandler LHP 20’s currently in the $2.60 to $2.70/lb range. Domestic LHP is in the $2.45 – $2.55/lb range and Combo Halves and Pieces in the $2.15/lb to $2.30/lb range. Chandler halves are in the $2.80 – $2.90/lb range. Many buyers are starting to come back from lockdown and while markets are generally quiet, buyers are very inquisitive as to where the markets are at price-wise and what can be had. Naturally buyers assume that packers are desperate to sell and trying to find cheap deals. New crop Inshell J/L Chandler seems to be in the $1.00/lb range with handlers telling us that it is not compelling to book lower prices than this unless they absolutely must. Lower prices than $1.00/lb would not allow a majority of growers to make their land payments and packers would be loathe to book deals putting the grower in this tenuous position.

Existing Inventory and sales position

Kernel seems to be in the hands of the larger handlers who typically hold goods all season. These handlers are not typically the cheap sellers and generally have a more regimented game plan. As discussed before, packers we talk to are truly 90-100% shipped and sold. We believe that while there is not a lot of Chandler inshell available now, packers are trying to figure out when to pull the plug on those higher priced export inshell sales and either resell the inshell or crack it. Inventory as a percentage of supply is about 24.2% but commitments against this inventory could well turn into kernels for sale. It is very hard to figure out who the players are that have most of the inventory.

The next 3 months for the fiscal season will be a challenge. We still feel that a carry out of 90,000 – 95,000 inshell ton is probable, this coupled with the recent Walnut Acreage Report (attached) which is reporting 365,000 bearing acres. Assuming highest per acre tonnage of 2.19 (2016) tons per acre would be 799,350 inshell ton. Assuming a more reasonable 2 ton per acre, would be 730,000 inshell ton. The packers we have talk to believe that new crop of 725,000 – 750,000 inshell ton is reasonable.

What We Know and Don’t Know

– What kind of demand will materialize over the last 3 months of the season? Can the industry get below a 90,000 ton carry-out?

– Chile’s 130,000 ton crop is slow to move out with the prices they are asking. How will Chile help or hurt California? Will they have an inordinate amount of inventory to cloud the picture for California at the time of California’s harvest?

– Cold storage has began in May 2020 but many packers we talk to do not have much to move out. Where is this remaining inventory? Who has it and what are they waiting for? How will California deal with inshell contracts not picked up as of yet? Will there be a rush to crack this inventory soon?

– What will the post Covid-19 world look like? While many of our buyers never closed, their customers like Airlines, Country Clubs, Restaurants, etc. are just starting to open up albeit with a myriad of restrictions. What will business look like going forward?

– Will governmental programs like the USDA Trade Mitigation and Commodity Solicitations that include walnuts continue and at what poundage level?

– What will the 2020-2021 new crop walnut crop look like. Will we have a record carry out with a record new crop on the trees?

CONCLUSION

The May 2020 MMR report/performance put the industry further behind in a very uncertain world. Many buyers are still trying to get through their existing contracts some at $.50 to $.80/lb above the prevailing market on a kernel basis. The inventory numbers suggest almost 16.5% of the crop remaining and 24.2% supply remaining (inclusive of carry-over) but as some advice, carry-over can be misleading as that is an accumulation of inventory over decades. With so many unknowns, pricing for new crop is a guess. Downstream demand is a guess too.