APRIL 2020 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

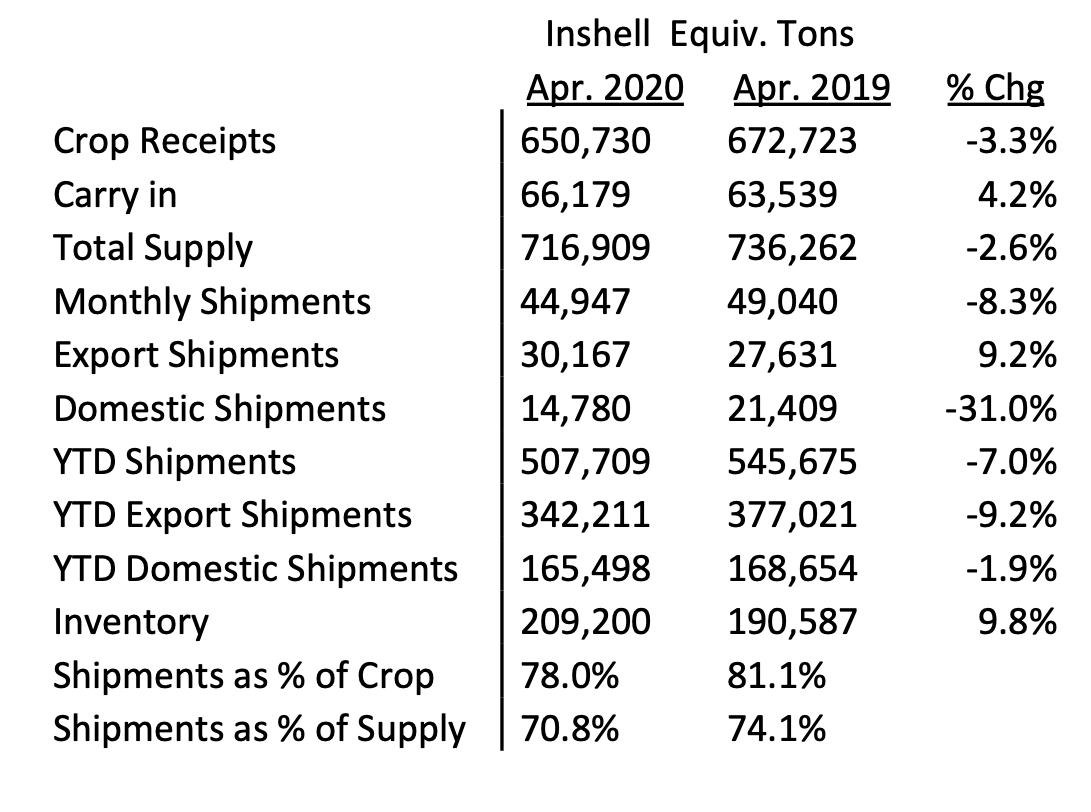

The California Walnut Board released the April 2020 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell (total) equivalent shipments -8.3% vs. PY

– Export inshell equivalent shipments +9.2% vs. PY

– Domestic inshell equivalent shipments up -31% vs. PY

2) Year to date inshell (total) equivalent shipments -7.0% vs. PY

– Export inshell equivalent YTD shipments -9.2% vs. PY

– Domestic inshell equivalent YTD shipments -1.9% vs. PY

3) Monthly inshell only shipments +9.56% vs. PY with Domestic -44.8% but Export +12.95%

– Key highlights include Turkey buying 4.1MM pounds from just a load in April 2019 but next to nothing from other countries

4) Monthly kernel only shipments -10.2% vs. PY with Domestic -31.1% and Export +8.1%

5) Year to date inshell only shipments -19.13% vs. PY with Domestic -36.4% and Export -18.3%. Inshell shipments of 269.7 million pounds is down by 63.8 million pounds from PY.

– Key highlights include YTD inshell shipments to Turkey very close to prior year at +1.2%, up 21.3% to India, -46.3% to UAE, +15.5% to Vietnam, +6.5% to Germany, +1.4% to Italy, -1% to Spain, -99.5% to Pakistan.

6) Year to date kernel only shipments -2% vs. PY with Domestic -0.7% and Export -3.0%. YTD kernel shipments are 328.1 million pounds or a decrease of 6.9 million pounds.

MMR DISCUSSION

As expected, April’s performance was soft at -8.3%. Inshell was not too bad at +9.56% but kernel was off -10.2% . Covid-19 and the 2-3 month lockdowns in many countries was, and still is, painful. This combined with the California walnut cold storage season starting and the shipping of new crop walnuts from Chile, adds pressure on California walnut packers to move goods just as we head in to the normally quiet summer months.

While packers were optimistic that sales would be decent for April due much cheaper prices, buyers are reeling from the decimation in bulk foods, restaurants, food service and leisure (cruise lines, air travel, retail and sporting events) and the resulting trickle down effect.

Covid-19

Not much more to say than what is already on the news. The virus has given buyers an open ended hall pass. Packers may still have many loads on contract undrawn at much higher levels and many are grasping at straws if they think that buyers, that have ignored please to pull their contracts, will magically put forth shipping instructions to pull those high priced loads. When will they throw in the towel? When will those goods come to market?

Chilean Walnuts

Chandler 30mm+ is between $2.60-$2.80/kg CFR. Chandler 20% LHP is around $7/kg CFR, 80% LHP is $7.60-$7.8/kg CFR and Hand cracked is between $10-10.50/kg CFR. Turkey is offering Chilean walnuts hand cracked in Turkey at $8.50/kg CFR.

Chile is having a slow start to their season as factories and shipping lines affected by Covid-19 and last year crop was 10 days earlier. It seems that Chile’s high prices has given USA an opportunity clear their stock. Chile’s percentage sold is being reported between 20-30%.

USDA Trade Mitigation and Domestic Commodity Solicitations

Thank heavens for the U.S. government. Did we just say that? Every bit helps and recently, there have been 3 Domestic Commodity Solicitations as follows:

1) Solicitation #1, 739K dried cherries, 972k raisins and 953K walnuts.

2) Solicitation #2, 10.2 million pounds of raisins, 3.2 million pounds of prunes, 8 million pounds of fruit and nut mix of which 1.6 million pounds is walnuts.

3) Solicitation #3 88k of dried cherries, 1.3 million pounds of cranberries 145,600 pounds of fruit mix (no walnuts), and 2.2 million pounds of raisins.

The walnut portion of solicitations 1 and 2 have drawn enormous interest from packers wanting to throw their hat into the ring. Packers that once had nothing available now are offering very large portions of this recent 2.5 million pounds of government walnut needs. There is talk that straight walnut buys as well as the fruit and nut mix with walnuts will become a monthly need up until new crop as much of this product goes into food banks and the demand is greater than ever. This would surely help as many packers eager to sell into these programs.

Inshell Prices and Kernel Prices

Inshell prices for Jumbo/Large Chandler still in the $.96/lb to $1.05/lb range. Again, when do packers off load Jumbo/Large Chandler currently on the books at $.25 – $.30/lb higher prices? Chandler LHP 20’s currently in the $2.55 to $2.70/lb range. Domestic LHP is in the $2.40 – $2.55/lb range and Combo Halves and Pieces in the $2.25/lb to $2.40/lb range. Chandler halves are in the $2.90 – $3.00/lb range. Markets are quiet with buyers bidding lower and lower on what small demand they may have. Many companies in select industries are still sheltering in place and have furloughed much of their staff.

Existing Inventory and sales position

Kernel material across the spectrum is available. Combo has become much more available as handlers finish up their packing season and as buyers “hand back” goods or are slow to pull goods that they cannot sell due to the “Covid-19” excuse. Many packers we talk to that had been 95-100% (shipped plus committed) now have goods to sell. While there is not a lot of Chandler inshell available, packers continue to wrestle with when to pull the plug on those higher priced export inshell sales and either resell the inshell or to crack it. Inventory as a % of supply is about 29% but commitments at this point are tenuous.

The next 4 months for the fiscal season will be a challenge. Last year, May – August 2018-2019 sales were 127,783 inshell ton. If we assume this number for the upcoming 4 months and subtract this number from existing inventory that would leave us carry out of 81,417 ton or an increase in carry out inventory of 23%. If during these 4 months we fall behind by 10% from last year’s sales, then the carryout would be approximately 94,195 or an increase of 42%.

What We Know and Don’t Know

– The crop is final at 650,730 ton.

– Chile’s crop is estimated to be 120,000 – 130,000 ton with inshell prices at about $1.20/lb to $1.27 CFR for Jumbo Large Chandler Inshell. We hear Chile’s crop is not their normal quality yet they have been slow to reduce prices. This stance should help California a bit.

– Cold storage has begun in May 2020 and will motivate packers to want to move goods out. How much motivation will they have?

– How will California deal with inshell contracts not picked up and how will they deal with push back by buyer’s on existing kernel contracts due to poor demand as a result of Covid-19? What will the post Covid-19 world look like? Will bulk business survive? Will food service and restaurant business ever be the same? Will hospitality (cruise lines, airlines and hotels) be the same? Will sporting events and amusement parks be the same?

– Can the USDA Trade Mitigation and Commodity Solicitations that include walnuts continue and at what poundage level?

– What will the 2020-2021 new crop walnut crop look like. Most pundits are confident that the crop will be over 720,000 ton as conditions were excellent. How will a record crop and a record carry-in affect prices?

CONCLUSION

The April 2020 MMR report did nothing to quell fears. In fact, Covid-19 questions are bigger than ever. Some packers are very well sold and have little to worry about. Some packers are not so lucky and will fight hard to get contracts shipped and growers paid but in an era of uncertainty where they are somewhat helpless to force the issue. We’ve heard new crop prices for inshell Chandler Jumbo/Large in the $1.00/lb range so that is a bit of a starting point.