January 2020 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

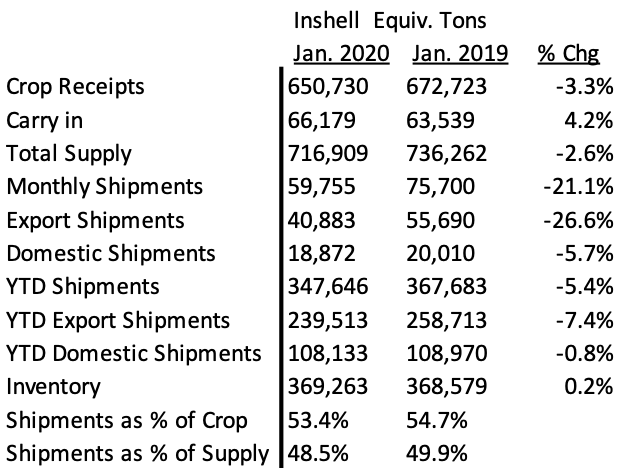

The California Walnut Board released the Jan. 2020 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell (total) equivalent shipments -21.1% vs. PY

– Export inshell equivalent shipments -26.6% vs. PY

– Domestic inshell equivalent shipments -5.7% vs. PY

2) Year to date inshell (total) equivalent shipments -5.4% vs. PY

– Export inshell equivalent YTD shipments -7.4% vs. PY

– Domestic inshell equivalent YTD shipments -0.8% vs. PY

4) Monthly inshell only shipments -56.36% vs. PY with Domestic -72.88% and Export -55.95%

– Key highlights include Turkey -74.1% vs. PY, Italy -42.32%, UAE -71.5%, Vietnam up 543%, India +98.5%

5) Year to date inshell only shipments -12.95% vs. PY with Domestic -35.19% and Export -11.83%

– Key highlights include YTD inshell shipments to Turkey up 6.14%, up 3.81% to India, -23.7% to UAE, -16.1% to Vietnam, +19.6% to Germany, +5.05% to Italy, +9.85% to Spain, -99.66% to Pakistan.

MMR DISCUSSION

This report verifies what the industry has been feeling the past month..…..a slowdown in sales across the board. This down performance combined with an additional 10,000+ ton of additional inshell walnut receipts makes for an increasing challenge for the California Walnut industry going forward.

To date, crop receipts of 650,730 inshell ton is now only -3.3% from PY 672,723 inshell ton receipts with total supply -2.6% vs. PY. This differs greatly from the opinions of some packers 4 months ago that believed tonnage would not surpass 600,000 ton. The 5 month YTD sales versus PY are -5.4% compared with last month’s (4 month) YTD sales which was -1.49%. This shows the industry losing ground yet current inventory is still -2.6% vs. PY. Recall that last year’s prices were significantly lower and monthly sales numbers higher due to prices that were about 30% lower on inshell and 25% on kernel. While this makes year over year monthly comparisons difficult, it does highlight what significantly higher prices can do to demand.

What a difference a month makes. Last month, with YTD inshell equivalent sales -1.49% but with a crop that was -4.54%, packers did not ring the alarm. After this month’s performance and more importantly the overall quietness pervading the industry, there is increasing concern. Some packers are hopeful that Chile’s drought will not put forth a bumper crop and lower prices. This should be a front burner topic of conversation at Gulfood this week. Other packers point towards China’s large crop and significant export sales being negatively impacted due to the Corona Virus and the resulting closure of some Chinese ports not allowing shipments to go out. Somewhat wishful thinking.

Inshell Prices and Kernel Prices

Inshell prices for Jumbo/Large Chandler have recently been done in the $1.30/lb range from about $1.15/lb at the start of the season and compared to last year of about $.95 – $1.05/lb. Chandler LHP 20’s currently in the $3.15 to $3.20/lb range. Domestic LHP is in the $3.00 – $3.05/lb range and Combo Halves and Pieces in the $2.90/lb to $2.95/lb range. Chandler halves are in the $3.50 – $3.60/lb range. Sales are quiet. As we said last month, the quietness can be deafening and packers don’t like the sound of it. When they are looking for drought concerns out of Chile or shipment issues out of China to help the Calif. Walnut Industry, there is concern.

Existing Inventory and sales position

Attached is the California Walnut Board 2019 Orchard Run Production by County, Variety and Percent of Crop. What we see is that the Chandler percentage of crop is 59.91 % and other varieties are 40.09%. If for 2020 we hold Chandler production steady at 389,838 ton and we revert the “other” varieties to the 2018 crop of 324,462 inshell ton, then the total would be 714,300 ton. Might this portend to be a forecast of what might be possible for 2020 or maybe more? This potential of what could be will also weigh on the minds of packers not wanting to carry over very much inventory at all.

At present, Chandler material is abundant. Packers do not seem to have an oversupply of combo or domestic light product but there are goods available to buy. Pieces are starting to become more available in light colour less so on combo. Packers had been content on packing to schedule but are looking for future months orders to fill in their schedule. Most packers we talk to are 80% – 90% sold which tells us that there are either some large packers or many small to medium packer’s or both that we don’t speak with that are undersold.

What We Know and Don’t Know

– The crop is mostly final at 650,730 ton.

– At Gulfood, Chile will put forth information on their crop, quality and no doubt look to book business but at what price?

– Inshell sales going forward will be very slow. When will packers begin to earnestly crack inshell and force feed the kernel market?

– What impact will the Corona Virus have on Chinese exports of walnuts if their ports are closed? Can they ship goods? Will a back-up in China reduce their already cheap prices once they begin to ship normally?

– India just raised the tariff on February 2, 2020 on US kernel from 30% to 100% (with Inshell already at 120%). What impact will this have on existing California walnut containers headed that direction? If there is trouble, packers will have to deal with the hardship of the “No Objection Certificate” if they (had not done so ahead of time) in order to re-export those containers elsewhere.

– Cold storage season will begin in April and will motivate packers to want to move goods out.

CONCLUSION

The January 2020 MMR report is seemingly bearish yet the North American market is only -0.8% behind PY and inventory is only up 0.2% but with much higher prices. California has clearly lost some momentum and is -5.4% YTD sales vs. PY. California only has “one tool in their toolbelt” to stop the trend and that is price. Their hope for facilitative news out of Chile and China is wishful but there is still about 8 months to go before new crop and plenty of time to right the ship and sell the crop, but most likely not at these prices.