December 2019 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

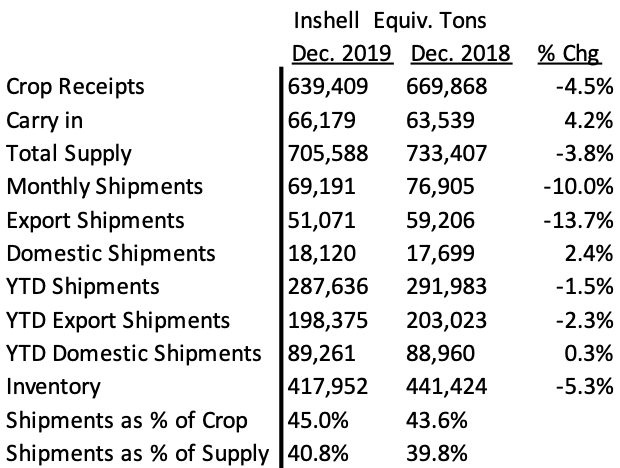

The California Walnut Board released the Dec. 2019 Position Report. Our table of these figures are shown below:

MMR and YTD HIGHLIGHTS

1) Monthly inshell equivalent shipments -10% vs. PY

– Export inshell equivalent shipments -13.7% vs. PY

– Domestic inshell equivalent shipments +2.4% vs. PY

2) Year to date inshell equivalent shipments -1.49% vs. PY

– Export inshell equivalent YTD shipments -2.3% vs. PY

– Domestic inshell equivalent YTD shipments +.34% vs. PY

MMR DISCUSSION

Bottomline, not great but not bad either. A relatively mundane report but depends on which side of the fence you are on which is always the case.

To date, crop receipts of 639,409 inshell ton is -4.54% from PY with total supply -3.8% PY. Commensurately, YTD sales are down -1.49% which is very understandable given the higher prices which we will compare later in this report.

We can see now that the 2019-2020 crop estimate of 630,000 ton has been exceeded with the 639,409 ton received in so far and no doubt will increase slightly with January 2020 receipts next month. The prior January 2019 received about 3,000 ton more so that is a pretty good approximation.

– Turkey’s inshell for Dec. 2019 was 14,418,056 pounds vs. prior year Dec. 2018 of 16,007,969 pounds so slightly bearish but 2018 inshell was much cheaper by about 30-40%.

– More importantly, Turkey inshell for November 2019 was 31,554,642 vs. 14,418,056 for December 2019; so a definite slowing in Turkish shipments and most likely the industry will not be able to count on Turkey much going forward. Packers that focus on inshell shipments will now turn their attention to kernel.

– Turkey’s YTD inshell sales represents more than one third of all YTD inshell shipments and 11.9% of total YTD shipments.

– Turkey’s YTD inshell sales are up 26.57% to a significant 75.4 million pounds from 59.6 million pounds last year.

– UAE inshell for Dec. was down 59.8% from PY but is on par YTD at 27 million inshell pounds for both 2018/2019 and 2019/2020.

– YTD Inshell to Germany up 22.26% with YTD Kernel up 80.66%. YTD Inshell to Europe up 12.5% and YTD Kernel up 19.9%.

– YTD Inshell to the Middle East/Africa is flat with PY and kernel is down 44% vs. PY.

– YTD Kernel to Asia is off 10.26% vs. PY with key markets Japan up 5.5% yet Korea down by -24%

YTD inshell equivalent sales are only off 1.49% with a crop that is approximately off 4.54% so with this performance, few packers are concerned. Most packer’s we talk to are 65-80% shipped and/or committed but since there are no “commitment” numbers in the MMR report, it is very hard to gauge the exact percentage “sold”.

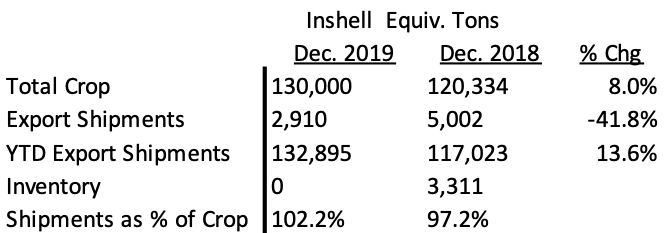

Chile

Chilenut released the December Walnut position report with a shipment of 2,910 tons compared to last year of 5,002 tons an decrease of 41.8%. YTD shipments are 132,895 tons compared to 117,023 tons last year an increase of 13.6%. YTD shipments to; UAE up 100%, Turkey down 22%, China up 76% and India down 32% compared to last year.

Chile is completely sold out. Chile will be a non-factor to the California Walnut Industry until Gulfood on 16th of February when new crop prices commence to be discussed.

Chinese Walnuts

The overseas markets would not seem to have an advantage buying out of CA and most likely will revert back to China to fill their upcoming requirements. Many overseas buyers are just getting some of their first Chinese shipments and have reported good quality. China is currently offering LAH80% USD4700, LH80% USD5400, LP USD5200 CFR. This may take California out of certain markets moving forward due to price.

Inshell Prices and Kernel Prices

Inshell prices for Jumbo/Large Chandler are still holding in the $1.40/lb range from about $1.15/lb at the start of the season and compare to last year of about $.95 – $1.05/lb. While Turkish shipments are down in December 2019 from both November 2019 and December 2018, Turkey has shipped a significant 75.4 million pounds YTD. Chandler LHP 20’s currently at a $3.35 to $3.40/lb range. Domestic LHP is in the $3.20 – $3.25/lb range and Combo Halves and Pieces in the $3.00/lb to $3.10/lb range. Chandler halves are in the $3.75 – $3.85/lb range. These prices seem to be about 30% – 35% higher than this time last year on both Kernel and Inshell. Buyer’s will make the argument that this year’s price is too high whereas packers will make the argument that last year’s prices were artificially low due to Chile still having decent amounts of inventory last year (Sept./Oct./Nov.) right when California was coming out with their new crop. CA Packers had to compete hard with Chile last year and much less this year. Chile will miss out on Ramadan which will be in April 2020.

Existing Inventory and sales position

While there seems to be an adequate and abundant amount of Chandler material to be had, Packers do not seem to have an oversupply of combo or domestic product. Additionally “pieces” of any color are in tighter supply. Packers are content on packing to schedule and have not seen any evidence or impetus from the numbers to lower prices. At around the 70% level that we believe the industry to be sold, they don’t seem too concerned about the remaining 30% with about 70% of the season to go.

What We Know and Don’t Know

– The crop will likely be finalized around 640,000 to 645,000 inshell ton or about approximately -4.5% down from the 2018-2019 crop. Buyers will continue to question the disparity between this decline in crop size and the approximately 30-35% price increase on inshell and kernel prices over last year’s prices at this time.

– Chile apparently has a drought they are dealing with and to what affect will this affect their crop? What price will be discussed in February 2020 at Gulfood?

– Inshell sales going forward will be slow. How will the diversion of inshell pounds to kernel affect the kernel market?

– What affect will China’s cheap walnut prices have on California? We hear that China’s product has had “good” to “mixed reviews” overseas on quality but will their cheap price be enough to keep buyers interested compared with California?

– With this performance, CA packers seem to be confident that they can ship this year’s crop fairly easily. Packer’s like to be at least 60% sold by now and seems they’ve achieved this at maybe 70%?

– Will YTD domestic shipments continue to be strong? Shipments are +.34% even with higher prices and still plenty of contracting needs going forward. Will the inevitable quietness in the walnut market after the holiday and into the Spring ring in the ears of packers who are not well sold and create any sort of panic?

CONCLUSION

The December 2019 MMR report is most likely a non-event with a slight bearish undertone which may lead to some room for better deals in the future.

Bottomline, the industry is down 1.49 % in shipments YTD but with a 4.5% smaller crop, it provides confidence to packers that the industry is at “Equilibrium”. Are we? We are in a quieter period and sometimes, the quietness can be deafening to packers. Conversely, Buyer’s would not be criticized for reading bearishness into this report creating the normal opposite sides of the fence that we’ve come to expect. We believe that there is still significant walnut needs that have to get booked domestically and overseas but to what extent will those needs get filled by cheap Chinese walnuts or by Chilean in May 2020?

We look forward to any questions, comments or interest you may have and we would be happy to assist you.