USDA/NASS has released the objective measurement report for the 2021/2022 crop year estimated at 670,000 tons. The full report may be found here: 202108walom_final.pdf (usda.gov). To say the least, this is a shocker to both buyers and sellers. The handlers will be meeting in Sacramento on Tuesday, September 7th to discuss opening prices for export and it will be interesting to see and hear the thinking behind these “export” price ideas and how to fairly price the product going forward. The forecast is based on 385,000 bearing acres, up only 1% from 2020’s estimated bearing acreage of 380,000 which no doubt reflects many acres removed. It also represents a meager 1.74 ton to the acre which is 10.3% lower than the 1.94 average ton per acre since 2007 and the 2.07 ton per acre this past year.

We will try to tie in all aspects of this market so you can see where we are at present:

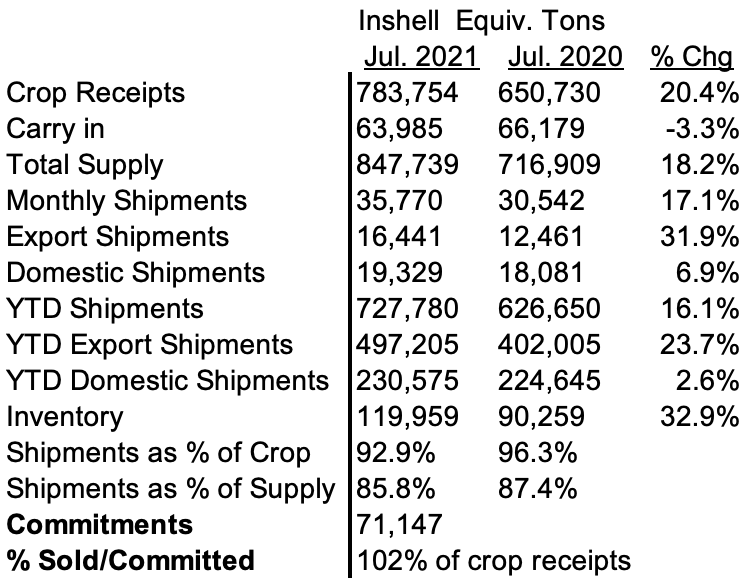

On August 10th the California Walnut Board released the July 2021 Position Report. Our table of these figures are shown below:

Commitments 3,486,312 Inshell pounds and 60,659,756 shelled pounds = 71,147 inshell equivalent tons

Total shipments plus commitments 798,927 inshell ton

% Sold/Committed 102% of crop receipts, 94% of total supply

MMR

July is the 11th month of the 2020-2021 walnut season. Through July is appears the industry is 102% shipped/committed based on crop receipts. The industry is 94% shipped/committed based on total supply.

Receipts are 783,754 inshell ton compared with the prior year at this time of 650,179 inshell ton as compared to the estimate of 780,000 ton. Shell out rate is estimated at 43.7% this year versus 42.6% last year. This shell out rate is a 60 month rolling average.

Most packers are sold out of some if not all kernel. What kernel is left will most likely be caught up in an updraft of higher prices due to today’s estimate and the pricing meeting on September 7th upcoming.

Current Inshell and Kernel Prices

Prior to today’s estimate, prices were approximately as follows: Chandler LHP 20’s currently in the $3.00 to $3.10/lb range with limited supply. Domestic LHP is $2.85/lb to $3.00/lb range. Combo Halves and Pieces in the $2.00/lb to $2.05/lb range. Chandler halves are virtually not available.

Chile

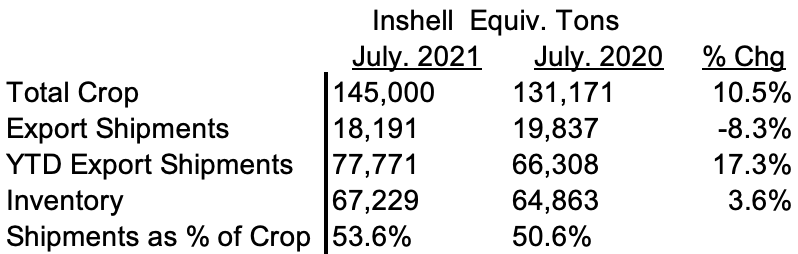

Chilenut released their July 2021 walnut position report (attached) with shipment of 18,191 tons compared to last year of 19,837 tons a decrease of 8.3%. Year to date; UAE up 33%, Turkey up 44%, China down 42% and India up 137% compared to last year. Chile so far shipped 53.6% of their crop and needs to ship additional 67,000 tons for this season.

Chilenut members are reporting 90% sold. Chile is currently not offering any walnuts. Only remaining inventory is industrial grade, light amber and yellow walnuts. Last 2 weeks vessels were cancelled due to bad weather. Last week Chile has seen good amount of rain and snowfall. Some Chilean farmers and exporters advised that they believe the snowpack holds enough water for them for next season yet there is another 7 months before they harvest Chandlers and much can happen. Chile will be a non-factor to California.

Transportation and Logistics

Transportation and Logistics continue to be a struggle with freight prices very high. Packers still are experiencing the shortage of vessels and containers and this situation most believe will be ongoing for another 12-18 months.

China

Below is an example of recent generic prices out of China. China’s prices on the surface are very cheap but freight out of China does erase some of the advantage.

Walnut Kernel 2021 New Crop

Extra Light Halves, $5350.00/mt Fob Qingdao, 185 Type Variety

Light Halves, $5040.00/mt Fob Qingdao, 185 Type Variety

Extra Light Halves, $5270.00/mt Fob Qingdao, Xin2 Type Variety

Light Halves, $4890.00/mt Fob Qingdao, Xin2 Type Variety

Light Halves, $4890.00/mt Fob Qingdao, Xinjian Mixed Type Variety

Light/Amb Halves, $3420.00/mt Fob Qingdao

Light/Amb Qtrs, $3270.00/mt Fob Qingdao

Walnut Inshell 2021 New Crop

185 Type Variety, 30mm+ $2520.00/mt Fob Qingdao

185 Type Variety, 32mm+ $2600.00/mt Fob Qingdao

185 Type Variety, 34mm+ $2750.00/mt Fob Qingdao

Xin2 Type Variety, 30mm+ $2280.00/mt Fob Qingdao

In the example above, Prices are offered FOB Qingdao. Estimated freight from China to Europe is around $700/mt or $.32/lb.

So if you look at line item above, Light Halves at $4890/mt or $2.22/lb plus $.32/lb = $2.54/lb. If you look at Inshell 30MM+ at $2,520/mt or $1.14/lb plus .32/lb = $1.46/lb from China to Europe. A Turkish client estimates that rail freight to Turkey from China is about $400.00/mt or $0.18/lb. Therefore, $1.14/lb plus $.18/lb = $1.32/lb which (prior to the estimate) compares to $1.35/lb Jumbo Large Chandler plus about $.08/lb freight to Turkey or $1.43/lb prior to the estimate. California can be higher on an FAS Turkey price but how much higher is acceptable? This is to give you an idea of competition from China to most of Europe and to Turkey.

What we know

– We know that current crop is largely sold out.

– We know that the new crop estimate is a disappointingly low number at 670,000 ton with minimal carryover whose quality composition is unknown. This estimate is the only number we will have until sometime in January 2022 after all the receipts are in.

– We know that Chile will largely be a non-factor to California as a competitor until after April 2022.

– We know that China will be a factor due their cheap FOB prices and while Chinese walnuts are different, the cheaper prices will be compelling to some users.

– We know Turkey is already buying significant amount of Chinese inshell walnuts.

– We know that the USDA domestic purchase commitments were 15.3 million pounds for 2020/2021 but that will be a question mark for 2021/2022 with the higher prices.

What we don’t know

– We don’t know where opening new crop price will start. The handlers will be meeting in Sacramento on Tuesday, September 7th to discuss opening prices for “export” and no doubt this will influence domestic prices as well. How high will prices rise?

– We don’t know the quality of the walnuts. The estimate does not speak to quality but many sellers have opined that the quality is good.

– We don’t know how many pounds will be needed by the USDA for their domestic purchases which were significant this past year. Higher prices should inversely hurt demand by the USDA,

The mantra for most packer’s is to try to stave off demand in order to get a handle on this market. There is no “chart” that anyone can look at that tells you where prices should be based on carry-over, crop size, quality and competition from abroad. Packers walk a fine line to try to balance supply and demand, get as much return for their growers as possible and to keep their customers in stock. This we know is not an easy task as they will always disappoint someone. The estimate leaves little room for growth, for the USDA to buy walnuts or for marginal customers to find walnuts. Those customers that have been loyal to a given packer or packers will be in the best position. One packer said it best saying “I am not taking on any unknown customers and will only sell to current customers”. The meeting on September 7th is only the first step in trying to establish pricing that we all can live with.