Nov. 2018 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

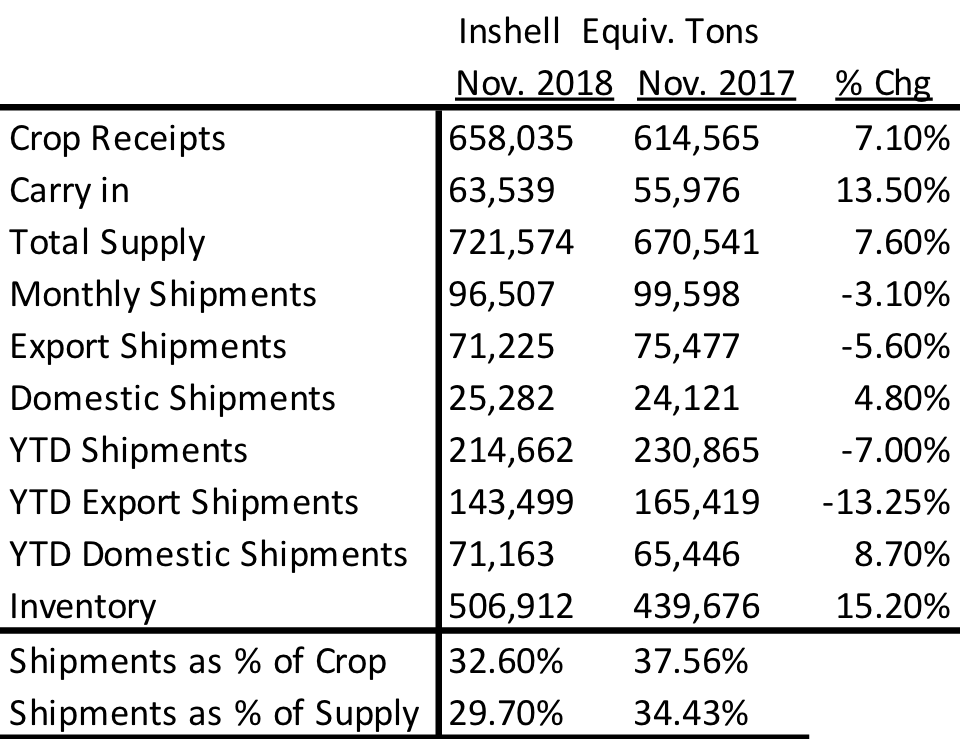

The California Walnut Board released the Nov. 2018 Position Report. Total November 2018 shipments were down 3.1% from prior year with Exports down 5.6% yet Domestic shipments up 4.8%. YTD shipments were down 7% with Exports down 13.25% yet Domestic shipments up 8.7%. Our table of these figures are shown below:

YTD shipments of 214,662 inshell equivalent ton compare negatively with the prior year by 7%. YTD export sales were down 13.25% compared with YTD Domestic sales which were strong up 8.7%. Trade wars may have taken a big bite out of export inshell sales as YTD export sales of 160 million inshell pounds were off 13.52% from the 2017 YTD Export Inshell sales of 185.6 million pounds. Many thought that the lateness to the start of the 2018 crop by about 2 weeks would “catch up” in November but this proved to be off base. While November domestic shipments held up by all accounts posting a gain of 4.8%, Export November 2018 shipments were off 5.6% a perplexing surprise to many as sales of inshell were felt to be brisk during November 2018 by many.

Crop Receipts are 658,035 ton compared to 614,565 ton prior year. Most handler’s believe that max 10,000 ton could be received in December 2018 so this crop should be roughly 3.5-4.5% short of the estimated 691,000 ton crop forecast.

USDA Trade Mitigation Program completed its first tranche of 6.125 million pounds for total dollar volume of $14.5 million for an average delivered price of $2.32/lb with another tranche solicitation in January 2019 for a similar amount. The amounts for the first tranche will be for deliveries December 16, 2018 through March 31, 2019 which will help the shipment numbers in those months.

Turkey purchased 26.47 million pounds in November 2018 compared to 23.67 million pounds the prior year or up 11.8%. Conversely, in October 2018 Inshell sales to Turkey were down 31.2% so there has been a turnaround from October just not as much as many would have hoped for and only 3 million pounds over the previous year’s November. So while Turkey was up in November, YTD total inshell sales to Turkey are still off 10%. Packers are optimistic that sales to Turkey in December will be year over year much better. Total export inshells sales for November 2018 were 77.8 million pounds vs the prior year of 76.26 million pound for November 2017 only up 2%. YTD export inshell sales of 160 million pounds are still down 13.5% from the 2017 YTD export inshell sales of 185 million pounds.

Germany – 2018 Year to date Kernel sales to Germany have been disappointing at 6.256 million pounds compared with 15.7 million pounds the same period last year or down 60%. Korea is down 12.8% and Japan is down 39% . YTD export kernel sales for the 3 month period ended November 2018 was 55.8 million pounds down 12.9% from the year earlier period which had sold 64.1 million pounds. On a brighter note, Domestic YTD kernel sales were up 11% at 58 million pounds, and in total were up 8.7%.

Chile will still be a strong competitor to California this upcoming season. As stated before, Chile will not want to be in the same position that they were this past season where they were long and seemed to have inventory up through September 2018. They will miss Ramadan sales for the foreseeable future and they should be aggressive in April 2019 with pricing and poised to ship strong in May 2019 assuming no issues with their crop.

Pricing for walnut material is as follows: Domestic LHP $2.20-$2.35/lb, Export quality 20% LHP $2.40 – $2.60/lb. CHP is in the $2.15lb to $2.30/lb range with many handlers being very short of material. Chandler Halves in the $2.60 to $2.70/lb range. Prior to today’s report, prices seem to be about $.10/lb higher than their earlier lows.

Conclusion– The only conclusion is that there is confusion. Many thought that the California WalnutIndustry would have a very strong November yet it was down 3.1% and down 7% YTD. Does the industry only have one tool in the toolbelt (price) to get back on track? Will the industry sell one pound more by dropping the price $.20/lb or would that have the affect to actually slow down sales as buyers wait for the product to be free? For now, this shipment report cannot help and will likely perpetuate buyer’s reluctance to jump in. Ironically many small and mid-size packers are completely swamped for the next two months and they were the ones that had the sense that November 2018 would be strong. Maybe the only conclusion is that some of the “larger” packers are undersold obscuring the fact that many small and mid size packers are 50-75% sold.