MARCH 2019 WALNUT MONTHLY MANAGEMENT REPORT AND DISCUSSION

The California Walnut Board released the March 2019 Position report. Our table of these figures are shown below:

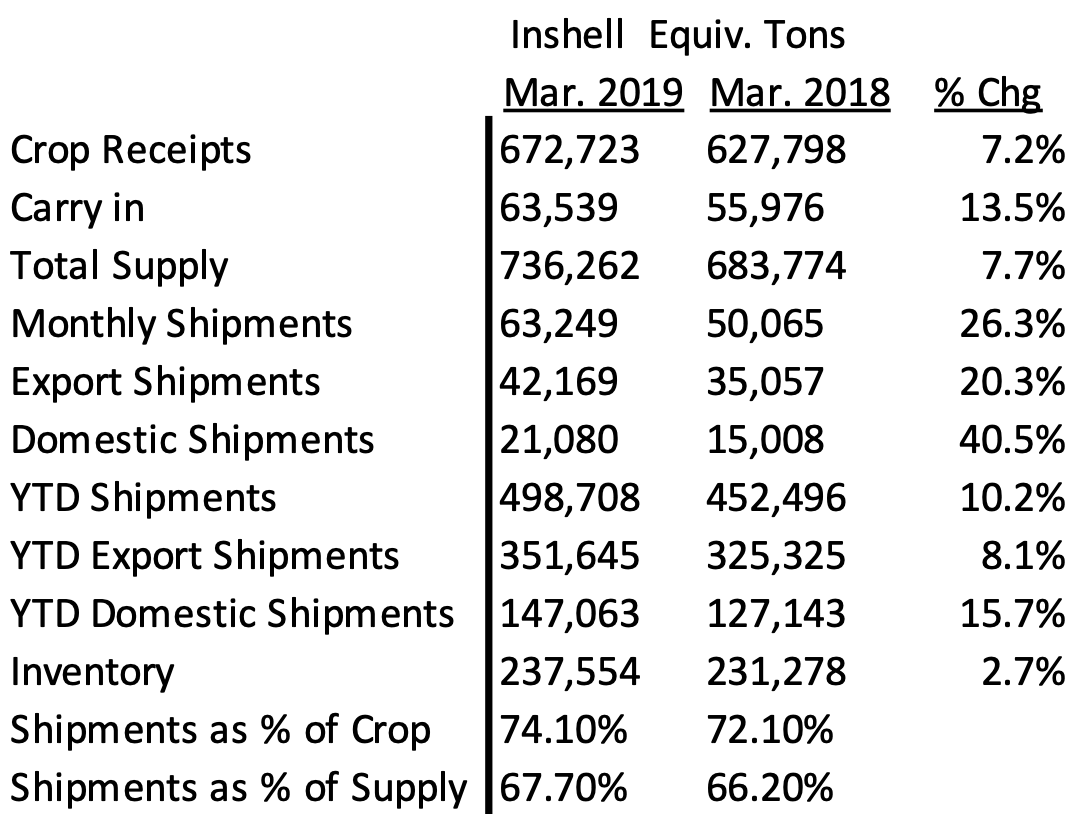

MMR and YTD HIGHLIGHTS

1) Monthly inshell equivalent shipments up 26.3% vs PY

– Export inshell equivalent shipments up 20.3% vs PY

– Domestic inshell equivalent shipments up 40.5%

2) Year to date inshell equivalent shipments now up 10.2% vs PY

– Export inshell equivalent YTD shipments up 8.1% vs. PY

– Domestic inshell equivalent YTD shipments up 15.6% vs. PY

MMR DISCUSSION

The Calif. Walnut industry had a very strong March 2019 up 26.3% over PY March 2018. This performance coming on the heels of a strong February 2019 which was up 35.9% over PY and a January 2019 up 38.7% against PY. Year to date March 2019 shipments are up 10.2% vs. PY with Export up 8.1% and domestic up 15.6% vs. PY.

Export Inshell YTD is up 15.2% with Domestic Kernel up 18.3% and Export Kernel up 3% YTD. As expected, Turkish inshell sales for March 2019 declined precipitously to 1.6 million pounds down from February’s number of 8.8 million pounds shipped. Turkey will pretty much be a nonfactor to California the remainder of the season as they bought a tremendous amount the past quarter and will be receiving Chilean inshell in the next couple of months. Italy, Pakistan and UAE all had significant inshell gains over PY March and that should slow down as well. Total March 2019 kernel sales were up 27.9% with Domestic up 43.6% and export up 20%. Chilean goods to ship in May will affect domestic kernel sales the rest of the season.

Analytical Discussion

For the next 5 months, April 2019 – August 2019, the industry needs to average 37,000 ton of sales per month to leave slightly less than the 2018 “carry in” of 63,539 ton amount as the 2019 “carry out”. This seems reasonable. The industry is already 74.1% shipped and with commitments, the industry seems to be over 90% shipped and/or committed. Commitments are an unknown as the industry does not report this number. While this percentage might lead to industry confidence, this 10% is still a significant amount of inventory and with some of the recent shipments made to traders and resellers, these goods need to move into an “end user” marketplace. Some of these goods are up for sale as we speak.

Other considerations

– Chile – Chandler harvest started at the end of last week which was 1 week earlier than expected. Early reports suggest that sizes are bigger this year compared to last year’s small size issues and the color is excellent. 1st chandler inshell shipments will commence next week. Chandler (JL) 30mm+ prices are stable between $2.80-$2.95/kg CFR. Serr is pretty much sold out and difficult to find offers, Serr (JL) 30mm+ prices are between $2.80-$2.85/kg CFR. Dubai has been a strong buyer of inshell while Turkey has been waiting for the harvest to cherry pick the best lots.

Chandler 20% LHP is $6.85-$7.10/kg CFR, 80% LHP is $7.45-$7.90/kg CFR and Hand cracked is $9.50-$10.50/kg CFR. Most packer are full for April and May shipments.

– Cold Storage – This is clearly on the minds of the packers in full force. Packer’s will try hard not to spend money for cold storage and maybe up for negotiation on goods rather than to expend additional funds.

– Pricing for walnut material is as follows has changed very little from last month: Domestic LHP $2.60 -$2.85/lb, Export quality 20% LHP $2.95 – $3.10/lb. CHP $2.45lb to $2.55/lb. Chandler Halves $3.30 to $3.50/lb range with minimal material available. Inshell material is pretty much non-existent.

Conclusion – The historical chart suggests that the industry is in a good and confident position. With reasonable assumptions, California seems to be on pace to oversell the crop and reduce the carry-out number to below that of the carry-in number. The question is whether our April and May forecast of 45,000 inshell ton is accurate or not. From a marketing standpoint, some good deals can be had on Domestic LHP and CHP on a nearby spot basis. A decent spread between domestic light halves and pieces and Chandler light halves and pieces is available if color and half count is secondary. Demand for April is a bit quiet with most buyers seemingly satiated for the time being or waiting for “cold storage” motivated deals to appear. Chandler LHP and Chandler Halves are stable and will mostly likely not decline in any meaningful amount.

We look forward to any questions, comments or interest you may have and we would be happy to assist you.